Book Appointment

Book Appointment

![]() March 20, 2026

March 20, 2026

![]() 0 Comments

0 Comments

![]() March 7, 2026

March 7, 2026

![]() 0 Comments

0 Comments

![]() February 21, 2026

February 21, 2026

![]() 0 Comments

0 Comments

![]() February 6, 2026

February 6, 2026

![]() 0 Comments

0 Comments

![]() January 17, 2026

January 17, 2026

![]() 0 Comments

0 Comments

![]() January 3, 2026

January 3, 2026

![]() 0 Comments

0 Comments

![]() December 27, 2025

December 27, 2025

![]() 0 Comments

0 Comments

![]() December 20, 2025

December 20, 2025

![]() 0 Comments

0 Comments

![]() December 13, 2025

December 13, 2025

![]() 0 Comments

0 Comments

![]() December 6, 2025

December 6, 2025

![]() 0 Comments

0 Comments

![]() November 29, 2025

November 29, 2025

![]() 0 Comments

0 Comments

![]() November 22, 2025

November 22, 2025

![]() 0 Comments

0 Comments

![]() November 14, 2025

November 14, 2025

![]() 0 Comments

0 Comments

![]() November 8, 2025

November 8, 2025

![]() 0 Comments

0 Comments

![]() November 1, 2025

November 1, 2025

![]() 0 Comments

0 Comments

![]() October 24, 2025

October 24, 2025

![]() 0 Comments

0 Comments

![]() October 11, 2025

October 11, 2025

![]() 0 Comments

0 Comments

![]() October 4, 2025

October 4, 2025

![]() 0 Comments

0 Comments

![]() September 27, 2025

September 27, 2025

![]() 0 Comments

0 Comments

![]() September 20, 2025

September 20, 2025

![]() 0 Comments

0 Comments

![]() September 12, 2025

September 12, 2025

![]() 0 Comments

0 Comments

![]() September 6, 2025

September 6, 2025

![]() 0 Comments

0 Comments

![]() August 29, 2025

August 29, 2025

![]() 0 Comments

0 Comments

![]() August 23, 2025

August 23, 2025

![]() 0 Comments

0 Comments

![]() August 16, 2025

August 16, 2025

![]() 0 Comments

0 Comments

![]() August 9, 2025

August 9, 2025

![]() 0 Comments

0 Comments

![]() August 2, 2025

August 2, 2025

![]() 0 Comments

0 Comments

![]() July 25, 2025

July 25, 2025

![]() 0 Comments

0 Comments

![]() July 19, 2025

July 19, 2025

![]() 0 Comments

0 Comments

![]() July 11, 2025

July 11, 2025

![]() 0 Comments

0 Comments

![]() July 4, 2025

July 4, 2025

![]() 0 Comments

0 Comments

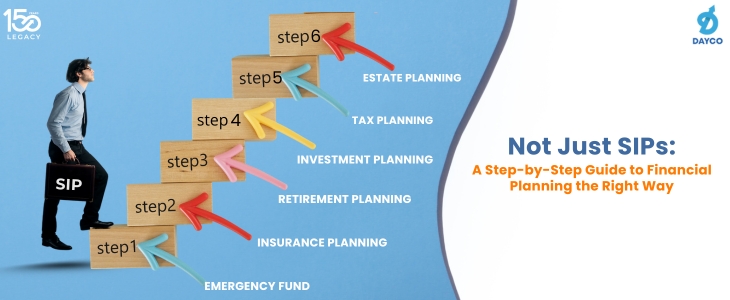

Go from unprepared to ready for anything with these seven easy steps to financial freedom and security.

Continue Reading![]() June 27, 2025

June 27, 2025

![]() 0 Comments

0 Comments

![]() June 21, 2025

June 21, 2025

![]() 0 Comments

0 Comments

![]() June 14, 2025

June 14, 2025

![]() 0 Comments

0 Comments

![]() June 7, 2025

June 7, 2025

![]() 0 Comments

0 Comments

![]() May 31, 2025

May 31, 2025

![]() 0 Comments

0 Comments

![]() May 24, 2025

May 24, 2025

![]() 0 Comments

0 Comments

![]() May 17, 2025

May 17, 2025

![]() 0 Comments

0 Comments

![]() May 10, 2025

May 10, 2025

![]() 0 Comments

0 Comments

![]() May 3, 2025

May 3, 2025

![]() 0 Comments

0 Comments

![]() April 26, 2025

April 26, 2025

![]() 0 Comments

0 Comments

![]() April 19, 2025

April 19, 2025

![]() 0 Comments

0 Comments

![]() April 12, 2025

April 12, 2025

![]() 0 Comments

0 Comments

![]() April 5, 2025

April 5, 2025

![]() 0 Comments

0 Comments

![]() March 28, 2025

March 28, 2025

![]() 0 Comments

0 Comments

![]() March 22, 2025

March 22, 2025

![]() 0 Comments

0 Comments

![]() March 14, 2025

March 14, 2025

![]() 0 Comments

0 Comments

![]() March 7, 2025

March 7, 2025

![]() 0 Comments

0 Comments

![]() February 28, 2025

February 28, 2025

![]() 0 Comments

0 Comments

![]() February 18, 2025

February 18, 2025

![]() 0 Comments

0 Comments

![]() February 8, 2025

February 8, 2025

![]() 0 Comments

0 Comments

![]() February 6, 2025

February 6, 2025

![]() 0 Comments

0 Comments

![]() February 1, 2025

February 1, 2025

![]() 0 Comments

0 Comments

![]() January 20, 2025

January 20, 2025

![]() 0 Comments

0 Comments

![]() December 20, 2024

December 20, 2024

![]() 0 Comments

0 Comments

![]() December 20, 2024

December 20, 2024

![]() 0 Comments

0 Comments

![]() December 12, 2024

December 12, 2024

![]() 0 Comments

0 Comments

![]() December 7, 2024

December 7, 2024

![]() 0 Comments

0 Comments

![]() November 22, 2024

November 22, 2024

![]() 0 Comments

0 Comments

![]() November 21, 2024

November 21, 2024

![]() 0 Comments

0 Comments

![]() November 14, 2024

November 14, 2024

![]() 0 Comments

0 Comments

![]() November 14, 2024

November 14, 2024

![]() 0 Comments

0 Comments

![]() November 8, 2024

November 8, 2024

![]() 0 Comments

0 Comments

![]() November 7, 2024

November 7, 2024

![]() 0 Comments

0 Comments

![]() November 5, 2024

November 5, 2024

![]() 0 Comments

0 Comments

![]() November 2, 2024

November 2, 2024

![]() 0 Comments

0 Comments

![]() October 26, 2024

October 26, 2024

![]() 0 Comments

0 Comments

![]() October 21, 2024

October 21, 2024

![]() 0 Comments

0 Comments

![]() October 11, 2024

October 11, 2024

![]() 0 Comments

0 Comments

![]() October 4, 2024

October 4, 2024

![]() 0 Comments

0 Comments

![]() September 27, 2024

September 27, 2024

![]() 0 Comments

0 Comments

![]() September 2, 2024

September 2, 2024

![]() 0 Comments

0 Comments

![]() September 2, 2024

September 2, 2024

![]() 0 Comments

0 Comments

![]() August 31, 2024

August 31, 2024

![]() 0 Comments

0 Comments

![]() August 17, 2024

August 17, 2024

![]() 0 Comments

0 Comments

![]() August 10, 2024

August 10, 2024

![]() 0 Comments

0 Comments

![]() August 10, 2024

August 10, 2024

![]() 0 Comments

0 Comments

![]() August 7, 2024

August 7, 2024

![]() 0 Comments

0 Comments

![]() August 3, 2024

August 3, 2024

![]() 0 Comments

0 Comments

![]() July 27, 2024

July 27, 2024

![]() 0 Comments

0 Comments

![]() July 22, 2024

July 22, 2024

![]() 0 Comments

0 Comments

![]() July 13, 2024

July 13, 2024

![]() 0 Comments

0 Comments

![]() July 8, 2024

July 8, 2024

![]() 0 Comments

0 Comments

![]() July 6, 2024

July 6, 2024

![]() 0 Comments

0 Comments

![]() July 4, 2024

July 4, 2024

![]() 0 Comments

0 Comments

![]() June 29, 2024

June 29, 2024

![]() 0 Comments

0 Comments

![]() June 22, 2024

June 22, 2024

![]() 0 Comments

0 Comments

![]() June 14, 2024

June 14, 2024

![]() 0 Comments

0 Comments

![]() June 8, 2024

June 8, 2024

![]() 0 Comments

0 Comments

![]() June 1, 2024

June 1, 2024

![]() 0 Comments

0 Comments

![]() May 24, 2024

May 24, 2024

![]() 0 Comments

0 Comments

![]() May 18, 2024

May 18, 2024

![]() 0 Comments

0 Comments

![]() May 18, 2024

May 18, 2024

![]() 0 Comments

0 Comments

![]() May 18, 2024

May 18, 2024

![]() 0 Comments

0 Comments

![]() May 13, 2024

May 13, 2024

![]() 0 Comments

0 Comments

![]() May 11, 2024

May 11, 2024

![]() 0 Comments

0 Comments

![]() May 4, 2024

May 4, 2024

![]() 0 Comments

0 Comments

![]() May 4, 2024

May 4, 2024

![]() 0 Comments

0 Comments

![]() April 29, 2024

April 29, 2024

![]() 0 Comments

0 Comments

![]() April 27, 2024

April 27, 2024

![]() 0 Comments

0 Comments

![]() April 27, 2024

April 27, 2024

![]() 0 Comments

0 Comments

![]() April 20, 2024

April 20, 2024

![]() 0 Comments

0 Comments

![]() April 13, 2024

April 13, 2024

![]() 0 Comments

0 Comments

![]() April 13, 2024

April 13, 2024

![]() 0 Comments

0 Comments

![]() April 11, 2024

April 11, 2024

![]() 0 Comments

0 Comments

![]() April 8, 2024

April 8, 2024

![]() 0 Comments

0 Comments

![]() April 2, 2024

April 2, 2024

![]() 0 Comments

0 Comments

![]() March 22, 2024

March 22, 2024

![]() 0 Comments

0 Comments

![]() March 21, 2024

March 21, 2024

![]() 0 Comments

0 Comments

![]() March 16, 2024

March 16, 2024

![]() 0 Comments

0 Comments

![]() March 10, 2024

March 10, 2024

![]() 0 Comments

0 Comments

![]() March 10, 2024

March 10, 2024

![]() 0 Comments

0 Comments

![]() March 10, 2024

March 10, 2024

![]() 0 Comments

0 Comments

![]() March 10, 2024

March 10, 2024

![]() 0 Comments

0 Comments

![]() March 9, 2024

March 9, 2024

![]() 0 Comments

0 Comments

![]() March 2, 2024

March 2, 2024

![]() 0 Comments

0 Comments

![]() February 24, 2024

February 24, 2024

![]() 0 Comments

0 Comments

![]() February 17, 2024

February 17, 2024

![]() 0 Comments

0 Comments

![]() February 10, 2024

February 10, 2024

![]() 0 Comments

0 Comments

![]() February 3, 2024

February 3, 2024

![]() 0 Comments

0 Comments

![]() January 27, 2024

January 27, 2024

![]() 0 Comments

0 Comments

![]() January 13, 2024

January 13, 2024

![]() 0 Comments

0 Comments

![]() January 6, 2024

January 6, 2024

![]() 0 Comments

0 Comments

![]() December 22, 2023

December 22, 2023

![]() 0 Comments

0 Comments

![]() December 18, 2023

December 18, 2023

![]() 0 Comments

0 Comments

![]() December 16, 2023

December 16, 2023

![]() 0 Comments

0 Comments

![]() December 9, 2023

December 9, 2023

![]() 0 Comments

0 Comments

![]() December 1, 2023

December 1, 2023

![]() 0 Comments

0 Comments

![]() November 25, 2023

November 25, 2023

![]() 0 Comments

0 Comments

![]() November 18, 2023

November 18, 2023

![]() 0 Comments

0 Comments

![]() November 11, 2023

November 11, 2023

![]() 0 Comments

0 Comments

![]() November 4, 2023

November 4, 2023

![]() 0 Comments

0 Comments

![]() October 28, 2023

October 28, 2023

![]() 0 Comments

0 Comments

![]() October 28, 2023

October 28, 2023

![]() 0 Comments

0 Comments

![]() October 14, 2023

October 14, 2023

![]() 0 Comments

0 Comments

![]() October 7, 2023

October 7, 2023

![]() 0 Comments

0 Comments

![]() September 30, 2023

September 30, 2023

![]() 0 Comments

0 Comments

![]() September 23, 2023

September 23, 2023

![]() 0 Comments

0 Comments

![]() September 16, 2023

September 16, 2023

![]() 0 Comments

0 Comments

![]() September 9, 2023

September 9, 2023

![]() 0 Comments

0 Comments

![]() August 31, 2023

August 31, 2023

![]() 0 Comments

0 Comments

![]() August 26, 2023

August 26, 2023

![]() 0 Comments

0 Comments

![]() August 19, 2023

August 19, 2023

![]() 0 Comments

0 Comments

![]() August 12, 2023

August 12, 2023

![]() 0 Comments

0 Comments

![]() August 5, 2023

August 5, 2023

![]() 0 Comments

0 Comments

![]() July 29, 2023

July 29, 2023

![]() 0 Comments

0 Comments

![]() July 28, 2023

July 28, 2023

![]() 0 Comments

0 Comments

![]() July 28, 2023

July 28, 2023

![]() 0 Comments

0 Comments

![]() July 28, 2023

July 28, 2023

![]() 0 Comments

0 Comments

![]() July 28, 2023

July 28, 2023

![]() 0 Comments

0 Comments

![]() July 22, 2023

July 22, 2023

![]() 0 Comments

0 Comments

![]() July 19, 2023

July 19, 2023

![]() 0 Comments

0 Comments

![]() July 15, 2023

July 15, 2023

![]() 0 Comments

0 Comments

![]() July 15, 2023

July 15, 2023

![]() 0 Comments

0 Comments

![]() July 15, 2023

July 15, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 10, 2023

July 10, 2023

![]() 0 Comments

0 Comments

![]() July 6, 2023

July 6, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 5, 2023

July 5, 2023

![]() 0 Comments

0 Comments

![]() July 4, 2023

July 4, 2023

![]() 0 Comments

0 Comments

![]() July 4, 2023

July 4, 2023

![]() 0 Comments

0 Comments

![]() July 4, 2023

July 4, 2023

![]() 0 Comments

0 Comments

![]() July 4, 2023

July 4, 2023

![]() 0 Comments

0 Comments

![]() July 4, 2023

July 4, 2023

![]() 0 Comments

0 Comments

![]() June 25, 2023

June 25, 2023

![]() 0 Comments

0 Comments

![]() June 24, 2023

June 24, 2023

![]() 0 Comments

0 Comments

![]() June 23, 2023

June 23, 2023

![]() 0 Comments

0 Comments

![]() June 22, 2023

June 22, 2023

![]() 0 Comments

0 Comments

![]() June 22, 2023

June 22, 2023

![]() 0 Comments

0 Comments

![]() June 22, 2023

June 22, 2023

![]() 0 Comments

0 Comments

![]() June 19, 2023

June 19, 2023

![]() 0 Comments

0 Comments

![]() June 19, 2023

June 19, 2023

![]() 0 Comments

0 Comments

![]() June 19, 2023

June 19, 2023

![]() 0 Comments

0 Comments

![]() June 19, 2023

June 19, 2023

![]() 0 Comments

0 Comments

![]() June 17, 2023

June 17, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 16, 2023

June 16, 2023

![]() 0 Comments

0 Comments

![]() June 15, 2023

June 15, 2023

![]() 0 Comments

0 Comments

![]() June 15, 2023

June 15, 2023

![]() 0 Comments

0 Comments

![]() June 15, 2023

June 15, 2023

![]() 0 Comments

0 Comments

![]() June 14, 2023

June 14, 2023

![]() 0 Comments

0 Comments

![]() June 14, 2023

June 14, 2023

![]() 0 Comments

0 Comments

![]() June 13, 2023

June 13, 2023

![]() 0 Comments

0 Comments

![]() June 13, 2023

June 13, 2023

![]() 0 Comments

0 Comments

![]() June 12, 2023

June 12, 2023

![]() 0 Comments

0 Comments

![]() June 10, 2023

June 10, 2023

![]() 0 Comments

0 Comments

![]() June 5, 2023

June 5, 2023

![]() 0 Comments

0 Comments

![]() June 5, 2023

June 5, 2023

![]() 0 Comments

0 Comments

![]() June 3, 2023

June 3, 2023

![]() 0 Comments

0 Comments

![]() June 2, 2023

June 2, 2023

![]() 0 Comments

0 Comments

![]() June 2, 2023

June 2, 2023

![]() 0 Comments

0 Comments

![]() June 2, 2023

June 2, 2023

![]() 0 Comments

0 Comments

![]() June 2, 2023

June 2, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() June 1, 2023

June 1, 2023

![]() 0 Comments

0 Comments

![]() May 31, 2023

May 31, 2023

![]() 0 Comments

0 Comments

![]() May 31, 2023

May 31, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 30, 2023

May 30, 2023

![]() 0 Comments

0 Comments

![]() May 24, 2023

May 24, 2023

![]() 0 Comments

0 Comments

![]() May 24, 2023

May 24, 2023

![]() 0 Comments

0 Comments

![]() May 24, 2023

May 24, 2023

![]() 0 Comments

0 Comments

![]() May 24, 2023

May 24, 2023

![]() 0 Comments

0 Comments

![]() May 19, 2023

May 19, 2023

![]() 0 Comments

0 Comments

![]() April 11, 2023

April 11, 2023

![]() 0 Comments

0 Comments

![]() March 27, 2023

March 27, 2023

![]() 0 Comments

0 Comments

![]() March 18, 2023

March 18, 2023

![]() 0 Comments

0 Comments

![]() March 13, 2023

March 13, 2023

![]() 0 Comments

0 Comments

![]() March 13, 2023

March 13, 2023

![]() 0 Comments

0 Comments

![]() March 10, 2023

March 10, 2023

![]() 0 Comments

0 Comments

![]() March 10, 2023

March 10, 2023

![]() 0 Comments

0 Comments

![]() March 10, 2023

March 10, 2023

![]() 0 Comments

0 Comments

![]() February 27, 2023

February 27, 2023

![]() 0 Comments

0 Comments

![]() February 27, 2023

February 27, 2023

![]() 0 Comments

0 Comments

![]() February 27, 2023

February 27, 2023

![]() 0 Comments

0 Comments

![]() February 23, 2023

February 23, 2023

![]() 0 Comments

0 Comments

![]() February 22, 2023

February 22, 2023

![]() 0 Comments

0 Comments

![]() February 22, 2023

February 22, 2023

![]() 0 Comments

0 Comments

![]() February 17, 2023

February 17, 2023

![]() 0 Comments

0 Comments

![]() February 17, 2023

February 17, 2023

![]() 0 Comments

0 Comments

![]() February 17, 2023

February 17, 2023

![]() 0 Comments

0 Comments

![]() February 16, 2023

February 16, 2023

![]() 0 Comments

0 Comments

![]() February 16, 2023

February 16, 2023

![]() 0 Comments

0 Comments

![]() February 16, 2023

February 16, 2023

![]() 0 Comments

0 Comments

![]() February 16, 2023

February 16, 2023

![]() 0 Comments

0 Comments

![]() January 13, 2023

January 13, 2023

![]() 0 Comments

0 Comments

![]() January 4, 2023

January 4, 2023

![]() 0 Comments

0 Comments

![]() December 19, 2022

December 19, 2022

![]() 0 Comments

0 Comments

![]() October 1, 2022

October 1, 2022

![]() 0 Comments

0 Comments

![]() August 13, 2022

August 13, 2022

![]() 0 Comments

0 Comments

![]() August 21, 2021

August 21, 2021

![]() 0 Comments

0 Comments

I'm a cool paragraph that lives inside of an even cooler modal. Wins!

In case you didn’t know, you can open your account online within 24 hours. Offline account opening takes up to 4 working days. If you wish to open your account offline, fill and sign the forms using a black/blue ballpoint pen. Please fill in the email and mobile number of the applicant to avoid account opening delays.

Please enter your details and password

New to Dayco?

Please enter your details and password

New to Dayco?

Your details were successfully received.

Our Team is working constantly on improving our user experience and your feedback really means a lot.

App Link Send to your mobile number successfully.

All your Questions have been recorded

All your Questions have been recorded

Thank you for your response. We'll get in touch with you at the earlisest for your investment planning needs

Thank You for your interest in our Moderate Equity Portfolio. Please find below the credentials to track this portfolio:

User ID: mockmod@daycoindia.com

Password: abcd@1234

Risk profiling is crucial for identifying and managing potential risks in investment decisions. Please carry out your risk profiling before making any investment decisions.

Please enter your details to download/print the report

Please enter your details to download/print the report

Please enter your details to download/print the report

Please enter your details to download/print the report

Please enter your details to download/print the report

Please Select an option from below

Please Select an option from below

We appreciate your interest in our services. Our team will be in touch with you shortly.

ClosePlease enter your details in the fields provided

Calculation report has been sent to your mail id successfully

This will remove your answers from all questions and cannot be undone.