Think beyond bank deposits to stave off Inflation

If you feel quite satisfied by keeping your savings in a bank or post-office fixed deposit scheme, think again. Sure, while signing up for a bank fixed deposit, you know beforehand exactly how much (rate of interest) and how long (the maturity of the deposit) you’ll get. But, have you considered the ‘real’ return on maturity after providing for inflation and income taxes?

Or, for that matter, bank fixed deposits also come with liquidity risks in the form that if you want to withdraw the money before maturity, you’ll have to pay a penalty.

Furthermore, your total deposit and accrued interest in a bank is insured upto Rs 5 lakh under the Deposit Insurance & Credit Guarantee Corporation Act. In other words, you stand to get back a maximum of Rs 5 lakh or your total deposit amount, whichever is less, when a bank goes bankrupt.

But the most potent enemy to any assured income scheme, including bank and post-office deposits, is inflation.

Inflation is the continuous and spiraling rise in prices of goods and services. Let us first understand how inflation is measured and then how it impacts your savings.

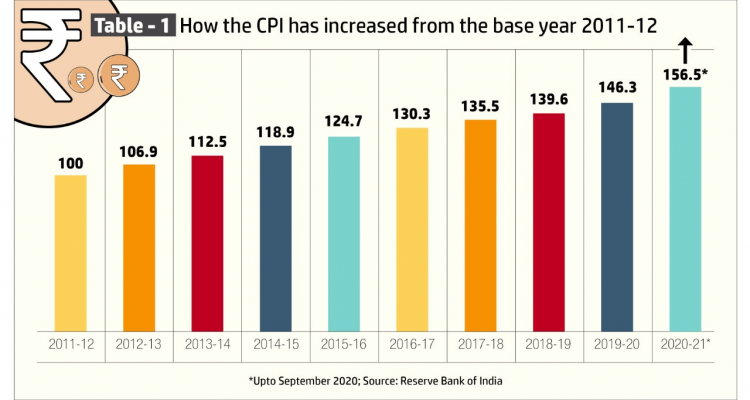

To measure inflation a year in the past is taken as a base year and the aggregate price level in that year is assumed as 100 to form the price index. The annual price indices for the following years when compared with the base year give us the annual rate of inflation. The table depicts the consumer price indices for each year starting from the base year 2011-12.

| Financial year | Consumer price index (CPI) |

| 2011-12 | 100 |

| 2012-13 | 106.9 |

| 2013-14 | 112.5 |

| 2014-15 | 118.9 |

| 2015-16 | 124.7 |

| 2016-17 | 130.3 |

| 2017-18 | 135.5 |

| 2018-19 | 139.6 |

| 2019-20 | 146.3 |

| 2020-21* | 156.5 |

Source: Reserve Bank of India

Here one can see, a commodity that was sold for Rs 100 in 2011-12 will now cost you Rs 156.50!

So, if a fixed deposit of Rs 100 made in 2011-12 doesn’t yield at least Rs 156.50 now, it would be a loss for you.

In 2012, the State Bank of India, for example, gave a maximum interest of 9.25% per annum on fixed deposits having maturities above one year and upto 10 years.

So, if you had kept Rs 100 in a SBI fixed deposit in 2012, it would have amounted to Rs 217.56 in the last eight and a half years.

But you won’t get that entire Rs 117.56 interest accrued in the last eight and a half years in hand, unless your annual income is below the income tax threshold.

If you fall in the 20% tax bracket, then you’ll have to pay an income tax of Rs 23.51 out of that Rs 117.56 accrued interest. You will get an interest of Rs 94.05 net of tax.

And, if you are in the 30% tax bracket, your net of tax interest will be Rs 82.29! (Here we have not calculated the 4% education and health cess).

So, by keeping your money (Rs 100) in a bank fixed deposit at an interest rate of 9.25% for eight and a half years, your real gain will Rs 37.55 (= 94.05 – 56.50) or Rs 25.79 (=82.29-56.50), depending on the income tax bracket you are in.

Would you still prefer a bank fixed deposit over other money making avenues? Think over.

If you have a question, share it in the comments below or DM us or call us – +91 9051052222. We’ll be happy to answer it.

– Parichoy Gupta