“SVB was not just a bank; it was the lifeline for startups,” said the Chief Financial Officer of one startup on the social media platform Reddit. Now that Silicon Valley Bank (SVB) has been shuttered, not only is the money of the startups stuck, venture capitalist-backed startups will now find it difficult to raise capital. The entire startup funding ecosystem is under threat.

But all this information concerns the startups in the United States. What about India? Will the collapse of the SVB negatively impact the growth of listed companies – especially those that depend on banking, financial services, and insurance (BFSI) sectors? What should YOU, as an investor in these Indian companies, do in order to protect your wealth? Let’s analyse.

Silicon Valley Collapse: What went wrong?

Silicon Valley Bank, founded in 1983 with its headquarter in California, USA, is a commercial bank primarily serving the innovation economy. Their financial services cater to technology and life science companies, venture capitalists, and private equity firms. SVB played a significant role in financing startups and emerging growth companies, with Apple, Cisco, and LinkedIn being top clients associated with the bank.

So what exactly went wrong with this bank? To understand this, one has to look at the chain of events that ultimately culminated with the fall of this bank. Let’s analyse –

What:

What Is the Root Cause of the Issue?

To say in one sentence, the decision of the leaders in Silicon Valley Bank to invest the money parked by startups in long-term bonds proved to be a wrong decision. Let’s delve deeper.

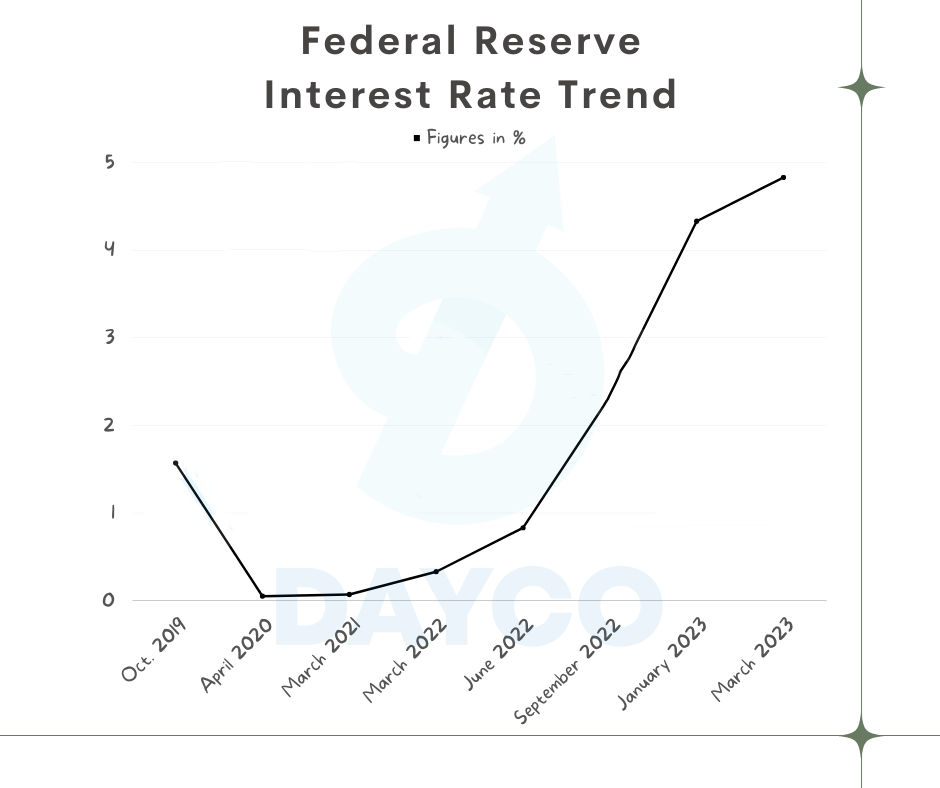

As the pandemic forced businesses across the United States to come to a standstill, the US government decreased the Federal Reserve Rates (Interest Rate) to almost zero. In 2019, the Fed Rate hovered around 1.5% to 2%. In 2020, the rate hovered around 0.5% to 0.9%. The rate stayed quite low even after the pandemic eased.

As a result of this low-interest rate, Venture Capitalists leveraged the low borrowing rates and invested more than they usually do in startups. Remember, these startups usually deposited the money in the Silicon Valley Bank, and the bank lent the money to startups. As a result, deposits in the bank increased from $62 billion to $190 billion within three years after the pandemic struck.

Now, this is where the Silicon Valley Bank made a wrong turn. Instead of investing the startups’ money in ultrasafe short-term government bonds, which are one of the safest instruments – in terms of market volatility, the bank invested the money ($91 billion, to be precise) in long-term mortgage-backed securities and bonds.

Why:

Why Was Investing In Long-Term Mortgage-Backed Securities a Bad Decision

The Silicon Valley Bank invested in long-term securities in order to get higher returns at a time when the interest rate was extremely low. However, from 2022 onwards, the Fed started increasing the Federal Reserve Rate at an unprecedented rate to calm US inflation which was at a 40-year-high. As a result, bonds like the one SVB invested in became more unattractive to investors. As the market interest rates increase, no one wants to keep holding bonds that pay lower, which decreases the price of bonds. As a result, the bonds held by SVB significantly lost their value.

How:

How Did This Decision Ultimately Result in the Fall of SVB?

As the interest rate kept climbing, money from VCs decreased. Startups needed funds from the banks as the venture funds dried up, which led them to start withdrawing money from the bank. To cater to these startups, the bank had to redeem its assets at a loss.

On the one hand, there was the possibility of Moody’s downgrading the bank’s credit rating, and on the other hand, SVB decided to raise money in order to continue providing cash to its customers. This spooked the startups. And thus began the frenzy of withdrawing money. This led to what is technically known as the ‘bank run’ – the scenario when a large number of a bank’s customers withdraw money simultaneously, causing banks to fail.- which is what happened with SVB, and on February 10th, 2023, the bank collapsed.

Will SVB’s wave of collapse hit the Indian coast? The Good News and The Bad News

Let’s start with the bad news.

Yes, there are startups in India – those that are backed by YCombinator, an American technology startup accelerator having huge exposure to the Silicon Valley Bank. According to this INC42 article, as many as 1000 Indian startups had so much exposure to SVB that they could have been forced to shut down if the crisis hadn’t been handled in a timely manner. Known names like Zepto or Meesho are rumored to have their cash stuck in SVB, although Meesho has vehemently rubbished the rumors. These Y-Combinator-backed startups – especially those that put all their ‘eggs’ in the same basket of SVB – will have a hard time recovering their money.

The Good News

Although many Indian startups will be feeling the ripple effect of the SVB collapse, Indian stock exchanges, overall, are resilient enough to withstand such short-term disruptions. Let’s look at how the bank failure affects (or does not affect) the Indian financial sector.

Banking Sector

The banking sector of India is cushioned up to face a near-zero impact. Experts believe the fall of SVB will most likely not have any noteworthy effect on the banking ecosystem of the country. This is because of the ironclad supervision of the Reserve Bank of India, making the banking system highly insulated and regulated.

Stock Market & Indian Investors

One thing about globalization is that any financial event, be it positive or negative, will cause a ripple effect in any known corner. As far as market sentiment is concerned, the second-largest bank failure has caused a massive uproar in the financial markets of the globe, including India. The Sensex, which surged by 250 points on the opening hours of March 13th, had a massive 1300-point plunge from the day’s high.

Stock market experts believe quotes of quality stocks falling might be a good opportunity for long-term positional investors, especially those who follow bottom fishing. Indian equity experts believe investments in quality auto, banking, and power sectors might be a good move.

Indian investors and lenders are at the edge of their seats, expecting a domino effect to develop anytime soon. However, they can consider themselves fortunate this time as the market participants monitoring the crisis have completely ruled out the chances of any significant obstructive effect on the Indian investor front.

A Note of Caution and a Possible Opportunity

Although most listed companies in India are immune to the SVB crisis, the WITCH (Wipro, Infosys, TCS, Cognizant, HCL) companies do have exposure to the BFSI sector in the US. And the overall banking and financial sector in the US is going through a slump. Around 30% of the revenues of these WITCH companies come from services provided to the BFSI sector. According to a recent report from JP Morgan, TCS and Infosys grabs the top spot in terms of exposure to SVB and other BFSI entities in the US.

As a result of this exposure to the BFSI sector in the US, investors who invested in these companies will see their returns decrease for a short period of time. This should be seen as a temporary blip. In fact, thanks to this crisis, the prices of these premium stocks will come down temporarily. This opens up the opportunity for investors to buy the stocks of these companies at lower-than-normal prices.

Bottomline: A Blip or a Break for India?

The crash of the US Bank is a “minor crisis” for India, as the government phrases it. The Indian government has undertaken immediate actions to help Indian startups. The process of depositing into Indian banks was executed flawlessly through collaborations of different arms of the government. There are no significant effects on the stock market of the country, unlike the turmoil in the US and UK markets.

In the U.S., it was feared that the collapse of the Silicon Valley Bank might have a domino effect on other banks. The “contagion effect” from the collapse of SVB did result in the collapse of Signature Bank in the US. However, the proactive measures taken by the U.S. government to ensure that depositors get their money back have reassured the market. The fact that First Citizens bought the collapsed Silicon Valley Bank in the last week of March has further reassured the citizens. The day after this sale took place, stocks of most banks opened in green. The situation is largely under control now, and many economists are also of the opinion that the US Fed would go very slow on the rate hikes, which is largely good news for the equity markets in India and US. With this, we will also see RBI going slow on the repo rate hikes. Hence, Indian investors can heave a sigh of relief. The likelihood of any contagion effect impacting the Indian stock market or the Indian banks is almost zero.

If you have a question, share it in the comments below or DM us or call us – +91 9051052222. We’ll be happy to answer it.

– Dipanwita Gupta